Quite recently, starting with version 3.0.43.50, in the 1C: Accounting 8 version 3.0 program, the developers added a new type of operation to the document “Correcting receipts” in the document Correcting own error. Now the document allows not only to register corrected or corrected invoices received from the supplier and to make appropriate adjustments in accounting, but also to correct technical errors made by accounting employees. In this article, using a specific example, we will consider in detail how you can correct in accounting and for tax purposes an error made when entering information from a primary document into the program.

Let me remind you that in order for the program to be able to use the documents Correction of receipt and Correction of implementation, it is necessary to enable the Correction and correction documents checkbox in the program functionality settings on the Trade tab.

Organization "Rassvet" applies the general tax regime - the accrual method and the Regulation on accounting (PBU) 18/02 "Accounting for calculations of corporate income tax." The organization is a VAT payer.

In January 2016, when entering into the program the primary document presented by a third-party organization of the act on the provision of services, the accountant made two mistakes. Firstly, he indicated the wrong cost of the service, and secondly, when registering the invoice received from the supplier, he made a mistake in specifying its number. An act on the provision of services received from the supplier is registered in the program using the document Receipt with the type of operation Services. In the “Amount” column of the tabular part of the document, instead of the correct 6,000 rubles, 5,000 rubles were indicated.

The received invoice is registered in the "basement" of the document by indicating its number and date. Instead of "real" number 7, number 1 was indicated.

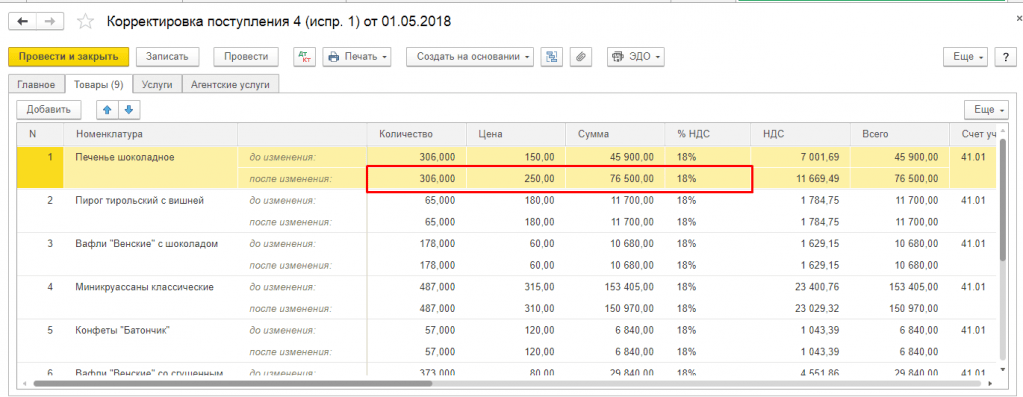

Expenses for the purchased service in accounting refer to general expenses (account 26). The document Receipt with the above errors and the result of its implementation are shown in Fig. one.

When carrying out the document in accounting and for tax purposes, I took into account the cost of services excluding VAT on the debit of account 26 "General business expenses", allocated on the debit of account 19.04 "VAT on purchased services" the amount of VAT presented by the supplier in correspondence with the credit of account 60.01 "Settlements with suppliers and contractors ”. Also, the document formed an entry in the VAT accumulation register presented, which is the basis for the formation of entries in the purchase book.

Consequently, as a result of an error in indicating the cost of the service in accounting and for tax purposes, the amount of expenses was underestimated, the amount of VAT charged was underestimated and the debt to the supplier was underestimated.

The document Invoice received is generated in the program on the basis of the document Receipt and, as a result, contains the wrong amount and amount of VAT.

Formed with an incorrect number, the Invoice received document is shown in Fig. 2.

In the program, the VAT amount can be deducted either with the help of the regulatory document Formation of purchase book entries, or directly in the Invoice received document, when the checkbox Reflect VAT deduction in the purchase book by the date of receipt is enabled.

The result of the document Invoice received is shown in Fig. 3.

The document, when carried out in accounting, accepted the VAT amount for deduction and formed an entry in the VAT register Purchases (in the purchase book), respectively, with an underestimated VAT amount and an erroneous invoice number.

The first quarter purchase book is shown in Fig. four.

The cost of the service was paid to the provider only in the next quarter. The Payment Order document was created on the basis of the erroneous Receipt document.

The posting of the corresponding document Write-off from the current account, created upon receipt of the statement from the current account, is shown in Fig. five.

Finally, as a result of a reconciliation of settlements with the supplier, this error was discovered in the second quarter. The VAT reporting for the first quarter has already been submitted by now.

Let us first recall how such a mistake should be corrected in accounting and tax accounting.

In accordance with clause 5 of PBU 22/2010 "Correction of errors in accounting and reporting", the reporting year error detected before the end of this year is corrected by entries in the corresponding accounting accounts in the month of the reporting year in which the error was detected.

In accordance with paragraph 1 of Art. 54 of the Tax Code of the Russian Federation, if errors (distortions) are detected in the calculation of the tax base relating to past tax (reporting) periods, in the current tax (reporting) period, the tax base and the tax amount are recalculated for the period in which these errors (distortions) were committed ...

True, there are exceptions to this rule. In accordance with the same clause of the Tax Code of the Russian Federation, the taxpayer has the right to recalculate the tax base and the amount of tax for the tax (reporting) period, in which errors (distortions) related to the previous tax (reporting) periods, when the mistakes (distortions) were made, led to excessive tax payment.

As we have already said, as a result of a mistake, the amount of expenses was underestimated. Consequently, for the purposes of taxation of profits, the taxable base (profit) was overstated and, accordingly, this led to an excessive payment of tax. Therefore, corrections for the purposes of taxation of profits can be made in the current reporting period, as in accounting.

But in order to figure out how we should deal with VAT, we will turn to the Decree of the Government of the Russian Federation No. 1137 of December 26, 2011. In accordance with clause 4 of the Rules for maintaining the purchase book, if it is necessary to make changes to the purchase book (after the end of the current tax period), the cancellation of the entry on the invoice, correction invoice is made in an additional sheet of the purchase book for the tax period in which the invoice, correction invoice, before making corrections.

To correct the error we have described, we will use the Document Correction of Receipt and select Correct our own error as the type of operation.

On the Main tab, you need to select the basis - this is the receipt document in which an error was made, which we will correct (in our case, this is the Receipt document (act, invoice) No. 1 dated January 11, 2016). Slightly below, when choosing the basis, the link to the corrected document Invoice received and its details is automatically reflected.

We need to correct the incoming number (the new value is 7). On this tab, you can choose where the adjustment will be reflected: only in VAT accounting or in all accounting sections (we want to make corrections to accounting, to income tax accounting and to VAT accounting). You can also select accounts to show income and expenses.

The completed Main tab of the Receipt adjustment document is shown in Fig. 6.

If, to correct an error, it is necessary to correct some sum indicators, then you may need the following tabs: Goods, Services, Agency services.

Since in our example a mistake was made when entering a certificate of service provision into the program, we will use the Services tab and indicate the correct price - 6,000 rubles.

The Services tab of the Receipt correction document is shown in Fig. 7.

When posting a document in accounting, it reverses the erroneous posting for VAT deduction (Dt 68.02 - Kt 19.04) in the amount of 900 rubles and will generate the correct posting in the amount of 1,080 rubles. In addition, it will allocate on the debit of account 19.04 the missing amount of VAT presented by the supplier (180 rubles), increase on the debit of account 26 "General business expenses" in accounting and tax accounting the amount of expenses for the service (1,000 rubles) and, accordingly, increase the amount owed on the credit of account 60.01 supplier (1 180 rubles).

The postings of the Receipt Correction document are shown in Fig. eight.

In addition to postings in accounting and tax accounting, the document will form entries in the VAT accumulation registers.

In the VAT register, the VAT charged (the amount of VAT charged by the suppliers) will be recorded for the correct amount of VAT, and since this amount of VAT is directly recorded in the purchase book by the document, its consumption will be immediately reflected.

Two records will be generated in the VAT register Purchases. The first entry is a cancellation of the VAT amount that was not legally accepted for deduction with an erroneous invoice number. And the second entry is the deduction of the correct VAT amount on the invoice with the correct details. Since corrections are made in the previous VAT tax period, the generated records will be marked with an additional sheet and the corresponding corrected period will be specified.

Formed by the document Correction of receipt of records in the accumulation registers are presented in Fig. nine.

Also, when posting a document in the program, a new invoice document will be created (registered) with the explanation “correction of your own mistake” (see Fig. 6). This document can be viewed in the list of documents Invoice received. The erroneous and corrected documents are shown in Fig. 10.

The form of the corrected document The invoice received contains the date of the correction and a link to the corrected document. Also in the form of the document there are the values of the details of the invoice received from the supplier before the error has been corrected and after it has been corrected (Fig. 11).

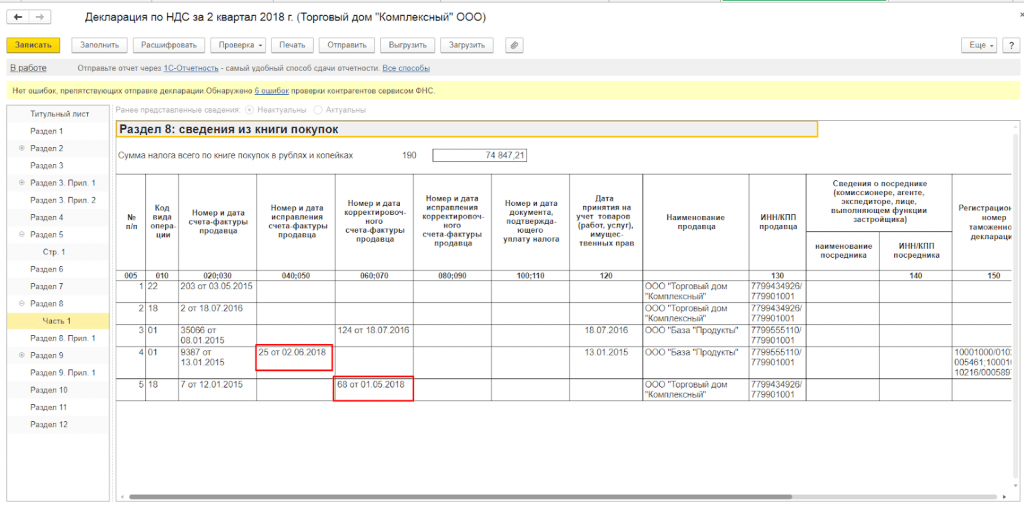

Let's, to check the correctness of our actions, create a purchase book for the first quarter - the tax period in which a mistake was made.

In the report we generate, we will indicate the required period. In the report settings, enable the "Generate additional sheets" checkbox and indicate the generation option - for the current period.

The settings for the Purchase book report are shown in Fig. 12.

Let's see an additional sheet of the shopping book.

As it should be, the additional sheet indicates the number of the additional sheet, the tax period and the date of compilation. Column 16 of the tabular section provides the total amount of VAT for the tax period before the additional sheet is drawn up.

The additional sheet contains, as we expected, two lines: an invoice reversal with incorrect numbers and amounts, and a revised entry with the correct invoice number and correct amounts.

An additional sheet of the first quarter purchase book is shown in Fig. 13.

The income adjustment is in many ways similar to the implementation adjustment, which is similar in purpose (see). In fact, the reflection of the document in the accounting is different due to the requirements of the legislation.

The document also has the ability to select two types of operations:

Correction in primary documents

... Adjustment by agreement of the parties

We can fix:

In the direction of decreasing or in the direction of increasing,

... documents of the current year and past years.

At the beginning of the article there is a step-by-step description of the work.- the sequence is the same for all situations. In the second part of the article, we will look at the details in more detail.

Step 1: We create a Receipt Adjustment based ondocument Receipt of goods and services that need to be corrected. We make the necessary edits and carry out. The second part of the article will describe in detail how to make corrections.

Step 2: Enter the invoice for hyperlink from Receipt Adjustments. The invoice must be recorded in order for the correction to be reflected correctly in the accounting and reporting in subsequent steps.

Step 3: After making any adjustmentsneed to start processingPosting documents for VAT registers.

This is usually done at the close of the month. This must be done before the formation of the records of the purchase or sales ledger, since the Receipt Adjustments do not perform the transactions themselves.VAT registers. If you do not start processing, the corrections will not go to the required sections of the sales or purchase ledger. Posting documents for VAT registers is launched from the Accounting Manager interface:

Step 4: For different transactions Receipt correction can be taken into account in additional sheetsshopping books or sales books. Therefore, in the next step, we need to make the documents Formation of purchase book records and Formation of sales book records. This is also a mandatory procedure at the end of the month.

To create these documents, it is convenient to use the Formation of VAT documents processing:

To start processing, specify the setting for generating VAT documents. In fact, this setting determines only manually or according to a schedule, the formation of documents should be performed. Here you can set up an automatic schedule. But now we will not do this and will start processing manually:

Step 5: Let's see how our adjustments were reflected in the buy and sell books.

Everything!

Now let's look at the details for the options:

We need to reduce the Receipt of goods and services issued in the previous quarter:

VAT reporting has already been submitted.

On the basis of the Receipt of goods and services, we will enter the document Receipt correction. 1C creates it with the operation type Correction of primary documents by default. Let's decrease the price one line at a time:

1C by default ticks the box Restore VAT in the sales book. I'll take it off.

The document generates transactions:

Fill in the data of the corrected supplier invoice according to hyperlink in the basement of the document.

We carry out the regulatory procedures for VAT specified in steps 3 and 4.

Posting documents to VAT registers adds a reversal of the VAT deduction toPosting the document Receipt Correction.

In the Formation of the book of purchases, we will form a record:

Now we can look at the result in the Shopping Book. We put a tick in the Generate add. sheets for the corrected period.

In the Main section, a new entry:

In the supplementary list, a complete correction of the entry for the corrected admission:

If we select the transaction type of the document Adjustment by agreement of the parties, then it will be possible to recover VAT in the sales ledger:

Here you need to select the Recover VAT in sales book check box In this case, we get the document postings:

After carrying out routine VAT transactions, we receive the following entries:

And VAT recovery in the sales ledger:

Adjustment with transaction type A downward adjustment by agreement of the parties is posted in the main section of the sales ledger in the adjustment period.

2. Adjustment of the current year receipts upward

The type of operation Correction of primary documents gives a similar result in the case of an upward correction of the receipt. We issue the Correction and the invoice:

We receive document transactions:

After performing routine VAT transactions, the transactions will look like this:

Correction with transaction type Correction in source documents reverses the amounts for the base document and creates a new entry in the period in which the correction is created.

Operation type Adjustment by agreement of the parties is reflected only additional accrual differences and is reflected in the main sheet of the purchase ledger in the adjustment period. Amounts reflected in the periodfoundation documentare not corrected.

Adjustment with transaction type An upward adjustment by agreement of the parties is posted in the main section of the purchase ledger in the adjustment period.

3. Adjustment of income from previous years

Correction of documents of receipts of previous years does not differ from adjusting receipts of the current year, except, perhaps, one nuance.

If we adjust the receipt of services, then for adjustments of the last year, on the Additional tab, it is necessary to indicate the item of income and expenses to which the difference will be attributed.

You may have missed a step. It is necessary to return to step by step description and check all items.

It happens that after the purchase of a product or its sale, it becomes necessary to adjust the written out primary. Such actions can be initiated by the supplier or the buyer if they discovered an error in the execution of the initial delivery documents, or by ourselves, for example, when any shortages or surpluses of goods were discovered during the acceptance of the goods.

Documents created and posted in a certain period can not in all cases, or at least be corrected correctly. For example, you cannot make changes to documents in a closed period: adjusting the receipts of previous years in 1C 8.3 may result in the reposting of many dependent documents, and as a result - distortion of the amounts of proceeds, taxes, etc. It is more correct to reflect this operation using separate documents provided in the 1C system.

You can make an adjustment after purchasing the required product through the document of the same name in "Purchases".

And also using the button "Create based on" directly from the receipt or manually add to the list of documents. In the case when a new document is created to change the implementation, then the delivery document, the data of which will be corrected, must be indicated in it.

If a correction document is entered on the basis of a delivery document, then the information on the corresponding receipt will be filled in automatically and there will be no need to drive it in manually. You can create the necessary documents "on the basis of", as an option, from the receipt document itself, or from their list.

In this case, on the "Goods" tab, the quantity and other numbers are copied to the "Before change" line from the original posted document upon receipt, therefore this line is not available for editing. The line "After change" is automatically filled in with similar values, but it is available for entering data that has been changed. You can change, decrease or increase the quantity of the accepted goods, as well as adjust the price if the price has changed unexpectedly, for example, while the goods were traveling from the supplier or the invoice operator entered erroneous data into the accounting system.

When you change the documents that formalize the receipt, there are also changes in mutual settlements with suppliers. At the same time, it is important not to forget to make changes to the VAT accounting.

For example, when correcting a receipt downward, you must select the "Restore VAT in the sales ledger" checkbox to restore the VAT previously recorded for deduction. After that, a corresponding record of the sales book is formed in the program. This becomes possible when choosing the type of the required operation "Adjustment by agreement of the parties." In this case, in the "Goods" the VAT rate is not available for change.

You can also specify in the document whether you want to reflect these changes in all relevant accounting sections or only make changes to VAT accounting. The transactions reflect the VAT recovery and record the item value adjustment data.

If the operation "Correction in primary documents" is selected, corrections will be directed to errors in primary documents. Here, to make adjustments, all columns of the tabular section are available for change. You can also generate VAT corrective movements.

Based on the selected purchase adjustment documents, you can create an Invoice Received. Data is entered by clicking the "Create on the basis" button from the document itself or from the list of documents for the purchase of goods.

When the cost of purchased goods increases, it is necessary to prepare a document "Formation of purchase book entries" and fill in the "VAT deduction" tab.

The button "Create on the basis" allows you to create a new document from the implementation or add it manually to the list of correction documents.

When a new document is created, if it was generated through "Add from the list of correction documents", you need to make sure that it contains the sales document whose data will be corrected.

When you change the sales data, not only settlements with the buyer are subject to change, but also the revenue, and, accordingly, the financial result of the company.

It is necessary to adjust the implementation downward in "1C: Accounting" in the same way as adjusting the receipt: select the operation (this can be either an adjustment by agreement or making the necessary corrections in the primary documents) and make changes to the quantity or cost of goods sold in the corresponding columns in the context each item of the item.

Similarly, we choose how to display the operation - in all relevant sections or in one VAT accounting. If you select "In all accounting sections", the adjustment generates movements in accounting and tax accounting, as well as movements in VAT accounting registers.

If you select "Only in VAT accounting", the movements are generated only according to VAT accounting registers, and in BU and NU you will have to reflect the adjustment manually. If you select Print Only, no movement is generated.

A corrective invoice can also be issued on the basis.

When creating records of the purchase book, there are corrective invoices according to the documents "Adjustment of receipts and sales".

When generating the regulatory report "VAT Declaration", which can be opened and generated in the "Reports" section, the automatically filled-in declaration includes the corrective invoices.

Thus, the 1C program has quite flexible and convenient mechanisms for reflecting various actions for the receipt and sale of products, the use of which will help to avoid accounting errors or lengthy re-conduct operations.

Thus, the 1C program has quite flexible and convenient mechanisms for reflecting various actions for the receipt and sale of products, the use of which will help to avoid accounting errors or lengthy re-conduct operations.

Step 1: We create the Implementation Adjustment Document through the input based on the Implementation of goods and services, which needs to be adjusted:

We fill out and post the document. We will return to the filling features below.

Step 2: Enter the invoice based on the Implementation Adjustment. The invoice ensures that subsequent steps are followed correctly and that the revised invoice is printed.

Step 3: We carry out processing Posting documents to VAT registers. This step is usually performed as part of month-end closing procedures. It cannot be skipped, since the Adjustment itself does not change the registers responsible for VAT accounting, which means that the sales and purchase books will not know about the existence of our changes without processing. Let's go to the Account Manager interface:

And we will perform processing for the selected period:

Step 4: Adjustments depending on the type of transaction can be posted either in the purchase book or in the sales book in additional sheets. In order not to miss anything, we always create Build Purchase Ledger Entries and Build Sales Ledger Entries. Also in the process of closing the month.

These documents can be created at a time by processing the Generation of VAT documents. In the same place, in the interface, the account manager we find the processing we need:

You will need to fill in the setting for generating VAT documents. But there is nothing complicated there: you need to fill in the name and organization. This setting can be used if you want to specify a schedule for automatic generation of documents. But you can not set a schedule, but start the mechanism manually:

Step 5: Form the buy and sell books themselves and check that all the adjustments are in the right places.

Now let's take a closer look at each case.

We need to reduce the implementation shipped in the previous quarter. VAT reporting has already been submitted on it.

At the first entry of the Implementation Adjustment 1C, 1C creates it with the operation type Correction of primary documents by default. Let's decrease the price one line at a time:

After carrying out, we receive the postings:

Do not forget to generate an invoice. It looks like this:

Then the document data should not be added to Formation of the purchase or sales ledger. Therefore, after posting documents to VAT registers, you can view the result in the Sales Book. We put a tick in the Generate add. sheets for the corrected period and look at the resulting additional sheet:

So,

Adjustment with transaction type A correction in the original documents reverses the amounts for the basis document and creates a new entry in the shipping period.

To achieve this effect, you need to change the operation type of the document to Adjustment by agreement of the parties:

In this case, we get the document postings:

As you can see, invoice 19.09 is involved - VAT on sales reduction. Such transactions are reflected in the purchase book. The invoice looks like:

1C will include these corrections in the Formation of the purchase book:

We carry out documents for VAT registers and form a purchase book for the adjustment period:

Adjustment with voucher type A downward adjustment by agreement of the parties is posted in the main section of the purchase ledger in the adjustment period.

Operation type Correction of primary documents gives a similar result in the case of an upward correction. The adjustment is reflected in the additional list of the Sales Ledger for the shipment period.

The type of operation A correction by agreement of the parties behaves differently. Let's increase the price on the first line of the document:

the document does not get into the Formation of Sales Ledger Records, but it is reflected directly in the main section of the Sales Ledger:

Adjustment with transaction type An upward adjustment by agreement of the parties is posted in the main section of the sales ledger in the adjustment period.

If you are making an adjustment, for example, for the last year, you need to determine whether the reporting has already been submitted or it is still possible to make adjustments. Depending on this, the system accounts for the transaction in different ways.

We will make adjustments by agreement of the parties. Go to the Additional tab and check the box if necessary:

If the period is closed, and we adjust to a decrease, then the system will issue the change through account 19.09 in correspondence with 91.1 other income:

If the flag is not set, the system will try to make all necessary adjustments on the last day of the last year:

In any case, the changes will be reflected in the purchase book during the adjustment period.

If we adjust to increase the amount, then the 19.09 account will be replaced by 68.02, and the adjustment itself will be reflected in the main section of the sales ledger for the period of the adjustment.

For the operation Corrections of primary documents, in any case, transactions will be issued through 68.02 and additional sheets will be filled in for the shipment period.

You have a broken sequence of actions somewhere. It is necessary

Taxpayers are often faced with situations when in the current tax period it is necessary to adjust or reflect the facts of economic life relating to past periods. This happens both through the fault of negligent managers who submitted the primary documents at the wrong time, and for objective reasons related to the terms of contracts, or based on the current business goal. Let us consider in specific situations how to reflect various options for adjustments affecting calculations for VAT, income tax, as well as accounting for past periods.

Adjustments related to the changein primary documents by agreement of the parties

There are four main types of such adjustments. This is a change in the value of goods sold (works, services, property rights) by agreement of the parties (in the direction of decreasing and increasing), as well as the provision of a discount, bonus or premium.

Situation 1. Decrease in cost

First, consider the situation when the cost of goods sold (works, services, property rights) changes downward.

Initial data

LLC "Alpha" in December 2014 accepted construction and installation work from LLC "Betta" in the amount of 1,180,000 rubles. (including VAT 18% - 180,000 rubles) and paid for them. In April 2015, as a result of the control measurement, outstanding, but paid work in the amount of 472,000 rubles was revealed. (including VAT 72,000 rubles). According to the organization's accounting policy, the materiality criterion is 5% of annual revenue. The revenue of the organization in 2014 amounted to 55 million rubles. Alpha LLC filed a claim and sent an additional agreement to reduce the contract price, which Betta LLC signed and paid in April 2015.

Accounting

The initial data describes a situation (a common practice in construction) when documents are drawn up for accounting for proceeds (work performed), although some of the work from this proceeds has not been done or has been done with process violations. Later, with various types of construction (audit) control, this is revealed and the amounts are "withdrawn" from construction contractors. In this case, there is an unjust enrichment (Chapter 60 of the Civil Code of the Russian Federation) from the contractor. That is, in accordance with PBU 22/2010 "Correction of errors in accounting and reporting" - an error in the form of dishonest actions of officials or misuse of information. According to the conditions of the example, the error is not material and is corrected by the buyer in accordance with clause 14 of PBU 22/2010, namely, the amount of previously recognized expenses is adjusted by recognizing other income in the form of the profit of previous years revealed in the current year.

In this case, the following transactions were initially issued in December 2014:

Debit 20 Credit 60

- 1,000,000 rubles. - reflects the costs of the work performed by the contractor on the basis of the signed act (clauses 5, 6.1, 16 PBU 10/99, article 254, clauses 3, clause 7, article 272 of the Tax Code of the Russian Federation);

Debit 19 Credit 60

- 180,000 rubles. - the presented VAT is reflected;

Debit 68 Credit 19

- 180,000 rubles. - VAT is accepted for deduction;

Debit 60 Credit 51

- 1,180,000 rubles. - paid for the work performed.

In April 2015, when the contractual obligations were changed on the basis of an additional agreement, the following entries were made:

Debit 76.2 Credit 91.1

- 400,000 rubles. - reflected other income in accordance with the supplementary agreement (clause 10.6, 16 PBU 9/99);

Debit 76.2 Credit 68

- 72,000 rubles. - VAT restored in accordance with the agreement;

Debit 51 Credit 76.2

- 472,000 rubles. - received funds for the claim.

For the purposes of tax accounting for income tax in the situation under consideration, expenses must be adjusted.

In accordance with para. 2 p. 1 art. 54 of the Tax Code of the Russian Federation, upon detection of errors (distortions) in calculating the tax base relating to past tax (reporting) periods, in the current tax (reporting) period, the tax base and the tax amount are recalculated for the period in which these errors (distortions) were committed. Consequently, in the tax declaration of LLC Alpha for 2014, the amount of tax payable was underestimated due to incomplete reflection of the information and the taxpayer is obliged to submit to the tax authority an updated tax declaration in accordance with Art. 81 of the Tax Code of the Russian Federation, to pay the missing amount of tax and corresponding penalties (clause 1 of Article 75 of the Tax Code of the Russian Federation).

Error or not? There is no concept of "error" in the Tax Code.

On the basis of paragraph 1 of Art. 11 of the Tax Code of the Russian Federation, the institutions, concepts and terms of civil, family and other branches of the legislation of the Russian Federation used in the Code are applied in the same meaning in which they are used in these branches of legislation, unless otherwise provided by the Code. And the rules for correcting errors in accounting are established by PBU 22/2010 (see Letter of the Ministry of Finance of Russia dated January 30, 2012 N 03-03-06 / 1/40). From the above, we can conclude that if some situation is not recognized as an error in accounting, then there is no error from the point of view of the Tax Code.

In accordance with PBU 22/2010, errors in the accounting sense should be considered as incorrect application of legislation, accounting policies, incorrect classification of the facts of economic activity, incorrect use of information, unfair actions of officials. But inaccuracies or omissions in the reflection of the facts of economic activity revealed as a result of obtaining new information are not considered errors. Thus, the accountant in each case must make a professional judgment about whether there is an error in accounting or not, and in accordance with this judgment, qualify the situation from the point of view of taxation.

LLC "Alpha" must also recover the amount of VAT previously accepted for deduction in accordance with paragraphs. 1 p. 2 art. 171, paragraph 1 of Art. 172 of the Tax Code of the Russian Federation, in the amount of 72,000 rubles. (subparagraph 4 of paragraph 3 of article 170 of the Tax Code of the Russian Federation), while the restoration is carried out on the earliest of the dates:

- the date of receipt by the buyer of primary documents for changes in the direction of reducing the cost of the work performed (additional agreement of the parties);

- the date of receipt by the buyer of the corrective invoice issued by the seller when the cost of the work performed changes downward (subparagraph 4, paragraph 3, article 170 of the Tax Code of the Russian Federation, paragraph 14 of the Rules for maintaining the sales book used in calculations for VAT, approved by the Decree of the Government of the Russian Federation from 26.12.2011 N 1137, hereinafter - Resolution N 1137).

Operations to adjust previously recognized income from sales are reflected in the accounting records in the month when the new circumstances of the transaction were determined, while the accounting records of the previous year are not adjusted (clause 80 of the Regulation on accounting and financial reporting of the Russian Federation, clause 6.4 PBU 9/99) ...

In this case, the seller must make the following transactions in April 2015:

Debit 91.2 Credit 62

- 472,000 rubles. - the loss of previous years, revealed in the reporting year, was recognized (clause 11 of PBU 10/99, Instructions for the use of the Chart of Accounts, clause 14 of PBU 22/2010);

Debit 68 Credit 91.1

- 72,000 rubles. - the tax deduction is reflected on the basis of the corrective invoice (paragraph 3 of clause 1, clause 2 of article 169 of the Tax Code of the Russian Federation).

Taxation at the seller (contractor)

A distortion of the tax base of the previous period leads to excessive payment of corporate income tax, therefore, in accordance with par. 3 p. 1 of Art. 54 of the Tax Code of the Russian Federation, the taxpayer has the right to recalculate the tax base and the amount of tax for the reporting period in which this distortion was revealed. In the situation under consideration - in April 2015. The taxpayer is not obliged to submit a revised tax return for 2014 (paragraph 2, clause 1 of article 81, subparagraph 1 of clause 2 of article 265 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated 23.03.2012 N 03-07-11 / 79).

The seller also issues a downward correction invoice within five calendar days from the date of preparation of documents (agreement, agreement, other) and accepts excess VAT deducted (clause 3 of article 168, clause 10 of article 172 of the Tax Code of the Russian Federation , Decision of the Supreme Arbitration Court of the Russian Federation of January 11, 2013 N 13825/12, clause 12 of the Rules for maintaining a purchase book used in calculating value added tax, approved by Resolution N 1137).

Situation 2. Increase in value

In a situation where the cost of goods sold (works, services, property rights) increases, when adjustments are reflected in accounting and tax accounting, the seller and the buyer change places.

As for VAT, the seller charges additional VAT on goods sold (works, services, property rights), and the buyer accepts VAT deduction in the tax period in which the documents for correction (agreements, correction invoices) were drawn up (clause 10 of Art. 154, Articles 168, 172 of the Tax Code of the Russian Federation).

Situation 3. Granting a discount

The condition for the provision of discounts, that is, the specific conditions for changing the prices of goods (work, services, property rights), and the procedure for documenting the buyer's right to discounts must be specified in the agreement (clause 2 of article 424 of the Civil Code of the Russian Federation).

Discounts are conditionally: provided in the past (retrodiscounts), present (reflected as a regular purchase and sale transaction based on the final sales price) and future (cumulative).

Discounts that change the price of goods arise either as a result of the purchase by the buyer of a certain amount of goods, or when purchasing goods for a certain amount, which means that it will be necessary to make adjustments to the primary documents already drawn up.

The main criterion influencing the procedure for reflecting adjustments is the period for granting the discount, namely before or after the end of the reporting year.

Initial data

In November 2014, OOO Sigma acquired ten units of equipment from OOO Gamma for the amount of 1,180,000 rubles. with VAT, and in December acquired five more for 590,000 rubles. in view of VAT. At the same time, in accordance with the contract, when the volume of purchases reaches 15 units, the price of all sold goods is reduced by 5% from the original.

Seller (contractor) accounting

In this situation, the conditions for granting a discount are fulfilled in one reporting period, it is necessary to adjust the sales proceeds and VAT based on the corrective invoice at the time of its provision.

Transactions in December 2014:

Debit 62 Credit 90.1

- 75,000 rubles. INVOICE - the revenue from previously shipped goods was reversed [(1,000,000 + 500,000) x 5%)];

Debit 90.3 Credit 68

- 13 500 rubles. INVOICE - VAT has been reversed on the amount of the discount provided [(180,000 + 90,000) x 5%)].

Let's change the initial data and agree that the achievement of the volume of purchases required to provide the discount took place in April 2015.

The transactions in April 2015 will be as follows:

Debit 91.2 Credit 62

- 75,000 rubles. - reflects the losses of previous years associated with the provision of discounts (clause 11 of PBU 10/99);

Debit 68 Credit 62

- 13 500 rubles. - accepted for deduction of VAT from the amount of the discount provided.

Seller taxation

A seller who has provided a discount in the form of a decrease in the price of a unit of goods (the cost of work, services, property rights) can adjust his tax liabilities for corporate income tax both for the period of sales of products with the submission of an updated declaration to the tax authority, and in the period of a decrease in the price of goods in accordance with the notice of a decrease in the price or approval of a change in the purchase price, since this operation led to excessive payment of tax during the delivery period (paragraphs 2, 3, paragraph 1, article 54, paragraph 2, paragraph 1, article 81 of the Tax Code of the Russian Federation, Letters of the Ministry of Finance of Russia dated June 29, 2010 N 03-07-03 / 110 , Federal Tax Service of Russia dated 17.10.2014 N ММВ-20-15 / [email protected]).

When granting a discount, the seller also issues a correction invoice to the buyer for the difference in value, in which you can indicate the change in prices for goods specified in several primary invoices (clause 2.1 of article 154, clause 3 of article 168, paragraph 2 clause 13 clause 5.2 of article 169, clause 4 clause 3 of article 170, clause 13 of article 171, clause 10 of article 172 of the Tax Code of the Russian Federation). The amount of VAT on the difference resulting from a decrease in the value of the goods can be deducted within three years if there are documents confirming the change in value (paragraph 3, clause 3, article 168, clauses 1, 2, article 169, p. 13 article 171, clause 10 article 172 of the Tax Code of the Russian Federation). There is no need to correct VAT calculations for the period of sale and to submit revised VAT returns.

The buyer's accounting also depends on whether a discount is provided before or after the end of the reporting year, and if the discount applies to purchased goods, then also on whether he managed to sell them and in what period it happened.

When selling goods (works, services, property rights) purchased at a discount in the previous reporting period, during the period of granting the discount, it is reflected in other income (clause 7 of PBU 9/99).

VAT from the amount of the discount granted is also restored in the period of granting.

When selling (writing off to production) goods purchased at a discount in the current reporting period, it is necessary to adjust its cost.

If materials are available in warehouses during the discount period, it is necessary to reduce the cost of the goods by the amount of the discount received, the amount of VAT accepted for deduction and mutual settlements with the seller.

Buyer (customer) taxation

For goods listed in warehouses during the discount period, their purchase value is recalculated (Letter of the Ministry of Finance of Russia dated 01.16.2012 N 03-03-06 / 1/13), and if the purchased goods have already been sold (this also applies to services received, works ), it is necessary to adjust the tax base for income tax for the tax period for recognizing expenses, including by recalculating the average cost of the relevant goods in tax accounting starting from the posting period until the time of writing off (Letters of the Ministry of Finance of Russia dated 16.01.2012 N 03-03-06 / 1/13, dated 20.03.2012 N 03-03-06 / 1/137, clause 8 of Article 254 of the Tax Code of the Russian Federation).

When granting a discount, the buyer should restore the resulting difference in VAT deduction to the earliest of the dates (as a rule, during the price adjustment period):

- the date of receipt of primary documents to reduce the price of goods;

- the date of receipt of the corrective invoice (paragraph 3 of clause 4 of paragraph 3 of article 170 of the Tax Code of the Russian Federation).

There is no need to correct VAT calculations for the period of sale and to submit updated VAT returns.

Situation 4. Provision of a bonus(provision of an additional batch of goods)

The condition for the provision of a bonus in the form of an additional supply of goods (work, services) for fulfilling the conditions on the volume of the purchase and the procedure for documenting the buyer's right to a bonus must be specified in the contract, as well as the fact that the cost of additional products is included in the total cost provided for by the contract ...

Accounting with the seller (contractor)

The actual cost of goods (works, services) transferred to the buyer as a bonus is included in the accounting as part of expenses for ordinary activities or as selling expenses (clauses 5, 7, 8, 9 PBU 10/99).

In tax accounting for income tax, expenses in the form of a bonus provided to the buyer for fulfilling the terms of the contract regarding the purchase of a certain volume of products (including those provided in kind) are recognized as non-operating expenses. Adjustment of the taxable base for income tax is not made (subparagraph 19.1 of paragraph 1 of article 265 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated 08.11.2011 N 03-03-06 / 1/729).

In order not to calculate VAT on the market value of the transferred bonus goods (works, services), as from donated in accordance with clause 2.1 of Art. 154 of the Tax Code of the Russian Federation, the taxpayer-seller must prove that "the price of the main product includes the cost of the additionally transferred goods and the tax calculated from the main operation also covers the transfer of additional goods" (clause 12 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation of 05/30/2014 N 33). To do this, it is necessary to enter into the agreement the most complete information on the accounting of the bonus.

Accounting with the buyer (customer)

In accounting, the bonus provided is reflected as part of other income (clauses 7, 9, 10.6, 16 PBU 9/99), and in tax accounting - as part of non-operating income (clause 10 of article 250 of the Tax Code of the Russian Federation). VAT is recorded as usual.

Situation 5. Granting a premium

It is advisable to specify the condition for the granting of the premium and the procedure for documenting the buyer's right to the premium in the contract and further draw up primary documents in accordance with Art. 9 of the Federal Law of 06.12.2011 N 402-FZ "On Accounting".

Accounting with the seller (contractor)

Accounting. If the terms of the contract do not provide for a change in the price of the supplied goods (work, services, property rights) as a result of the payment of the premium, the amount of the premium provided is recognized as an expense for ordinary activities (for example, as selling expenses) in the reporting period in which the organization has an obligation to the buyer in the amount of the premium provided (clauses 5, 16, 18 PBU 10/99). According to the rules, there is no adjustment to previously recognized sales revenue by the amount of the premium (clause 6.5 of PBU 9/99).

In tax accounting for income tax, the premium is accounted for as non-operating expenses at the date of their submission in relation to:

- goods - on the basis of paragraphs. 19.1 clause 1 of Art. 265, pp. 3 p. 7 art. 272 of the Tax Code of the Russian Federation;

- works, services - on the basis of paragraphs. 20 p. 1 art. 265 of the Tax Code of the Russian Federation (Letters of the Ministry of Finance of Russia dated 20.10.2014 N 03-03-06 / 1/52651, dated 07.04.2014 N 03-03-06 / 1/15487).

In a situation where the seller's transfers to the buyer of a premium (remuneration) for achieving a certain volume of purchases (ordered works, services) do not change the value of previously supplied goods (works, services), the seller has no grounds for adjusting the VAT tax base (Letter of the Ministry of Finance of Russia dated 24.04. 2013 N 03-07-11 / 14301).

If the amount of the premium provided entails a decrease in the cost of the goods (work, services) shipped, then after drawing up a document confirming the buyer's right to receive a premium (act, notification, protocol, etc.), the seller must issue an adjustment invoice to decrease and register it in the purchase book of the current period (Resolution N 1137).

Please note: in terms of the sale of food products, the amount of the premium should not exceed 10% of the price of the goods purchased by the buyer (clause 4 of article 9 of the Federal Law of December 28, 2009 N 381-FZ "On the Basics of State Regulation of Trade Activities in the Russian Federation") ... The payment of the premium is not allowed in terms of the sale of goods specified in the Decree of the Government of the Russian Federation of July 15, 2010 N 530.

Accounting with the buyer (customer)

In accounting, the bonus provided is reflected in other income (clauses 7, 9, 10.6, 16 PBU 9/99).

In tax accounting for income tax, it is advisable for the buyer to include the received remuneration (premium) in the structure of non-operating income (Letter of the Ministry of Finance of Russia dated August 26, 2013 N 03-01-18 / 35003). At the same time, there is no such requirement directly in the RF Tax Code.

If the received premium (remuneration) for achieving a certain volume of purchases does not change the value of previously supplied goods (works, services), then the buyer has no grounds for recovering the amount of tax deductions for VAT (Letter of the Ministry of Finance of Russia dated 04.24.2013 N 03-07-11 / 14301).

But if the received amount of the premium entails a decrease in the value of the goods (works, services) shipped, it is necessary to adjust the amount of VAT deduction and register an adjustment invoice from the seller in the sales book of the current period (Resolution No. 1137).

Please note: the premium paid under contracts for the supply of food products does not change the value of previously delivered products, which means that the seller and the buyer do not need to adjust the tax base (Letter of the Ministry of Finance of Russia dated 09/18/2013 N 03-07-09 / 38617, clause 4 of Art. . 8 Federal Law of 28.12.2009 N 381-FZ).

Reflection of documents received late

Accounting

The procedure for reflecting business transactions on documents received late depends on when they were received (PBU 22/2010):

- before signing the financial statements;

- after signing and submitting financial statements, but before approval;

- after the approval of the financial statements;

as well as on the level of materiality (the organization determines the materiality independently, see, in particular, Letter of the Ministry of Finance of Russia of 24.01.2011 N 07-02-18 / 01).

"Insignificant" documents are reflected in the reporting period in which they were received (clause 14 of PBU 22/2010), by entries:

Debit 60, 62, 76 Credit 91.1

- unreported income (excessive expense) was identified;

Debit 91.2 Credit 10, 60, 62, 76

- an unreported expense (excess income) has been identified.

"Material" documents received after the approval of the annual accounts are reflected in the current reporting period. Adjustment of the approved reporting is not made (clause 39 of the Regulations on accounting and reporting, clause 1, clause 9, clause 10 of PBU 22/2010). In this case, postings are drawn up:

Debit 62, 76, etc. Credit 84

- unreported income (excessive expense) of the previous period was revealed;

Debit 84 Credit 60, 76, 10, etc.

- revealed unreported expense (excess income) of the previous period;

Debit 84 Credit 68

- additional tax on profit of the previous period was charged according to the revised declaration;

Debit 68 Credit 84

- the income tax for the last year was reduced according to the revised declaration.

In accordance with clauses 4, 7 of PBU 18/02, depending on how tax accounting is corrected (or not corrected), it is necessary to reflect either permanent tax liabilities (Debit 99 Credit 68) or a permanent tax asset (Debit 68 Credit 99).

"Material" documents received after the signing and submission of financial statements, but before their approval, are corrected by entries for December, and the financial statements must be replaced with an indication of the reasons for their replacement (clauses 6, 7, 8, 15 PBU 22/2010 ).

Taxation

Failure to reflect business transactions in the past period is an error that led to distortion of data for past periods. Therefore, upon receipt of supporting documents (clause 1 of Art. 252 of the Tax Code of the Russian Federation) and in accordance with Art. Art. 54, 272 of the Tax Code of the Russian Federation, by the Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation of 09.09.2008 N 4894/08:

- with an increase in the amount of income relating to the previous period, an updated tax declaration is submitted for the period to which the adjustment relates (paragraph 2, clause 1 of article 54 of the Tax Code of the Russian Federation);

- with an increase in the amount of expense relating to the previous period, the taxpayer has the right to choose (paragraph 3, clause 1, article 54, paragraph 2, clause 1, article 81, subparagraph 3, clause 7, article 272 of the Tax Code of the Russian Federation, Resolutions of the FAS Of the North-Western District of 05.06.2012 N A44-3816 / 2011, of 31.01.2011 N A56-10165 / 2010, of the North Caucasian District of 22.02.2012 N A53-11894 / 2011, of the Moscow District of 03/15/2013 N A40- 54227 / 12-90-293, dated 14.08.2013 N A40-110013 / 12-20-566, the Ninth Arbitration Court of Appeal dated 26.03.2013 N 09AP-6639/2013, Letters of the Ministry of Finance of Russia dated 23.01.2012 N 03-03- 06/1/24, dated 25.08.2011 N 03-03-10 / 82, Federal Tax Service of Russia dated 11.03.2011 N KE-4-3 / [email protected]):

submit an updated tax return for the period to which the primary accounting document relates;

or adjust the taxable base in the current tax period (year).

Features not to be missed

The taxpayer has the right to adjust the taxable base of the current period only if in the period to which the error relates, the taxpayer has a profit according to tax accounting data. If, according to tax accounting data, a loss is obtained, then there is no fact of excessive tax payment, therefore, an updated tax declaration is submitted (Letters of the Ministry of Finance of Russia dated 30.01.2012 N 03-03-06 / 1/40, dated 05.10.2010 N 03-03- 06/1/627, dated 11.08.2011 N 03-03-06 / 1/476, dated 15.03.2010 N 03-02-07 / 1-105).

If the costs of the previous period are reflected in the primary document drawn up and received in the current tax period, for tax accounting purposes, the costs of such a document will be considered current, since the date of drawing up the document is a fundamental condition for reflecting business transactions (clause 2 of Art.272 Tax Code of the Russian Federation, Letters of the Ministry of Finance of Russia dated December 14, 2011 N 03-03-06 / 1/824, UFNS for Moscow dated December 22, 2011 N 16-15 / [email protected]).

If the date of signing the primary document by the customer refers to the next reporting period, the difference in tax accounting will arise depending on what kind of relationship arose under the contract - the provision of services or the performance of work:

- when services are provided and there is evidence of their provision, revenue and VAT are reflected by the date of the act, i.e. on the date on which the customer has the obligation to pay for the services received, and does not depend on the date of signing the act by the customer (clause 5 of article 38, clause 1 of article 39 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated 13.11.2009 N 03-03- 06/1/750, Determination of the Supreme Arbitration Court of the Russian Federation dated 08.12.2010 N VAS-15640/10, Letter of the Federal Tax Service of Russia for Moscow dated 30.04.2008 N 20-12 / 041989), and the customer recognizes costs for tax purposes not earlier than the date signing the act of services rendered;

- when performing work to reflect the proceeds, VAT from the contractor and the costs of the customer, it is the date of acceptance of their results (the date of signing the act) by the customer that matters (clause 1 of article 720 of the Civil Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated March 16, 2011 N 03-03- 06/1/141).

VAT accounting

Upon receipt of an invoice from the seller and the fulfillment of other conditions provided for in Art. 172 of the Tax Code of the Russian Federation, the buyer has the right to apply the tax deduction.

When receiving an invoice in a later tax period, the taxpayer does not have any errors and distortions in the calculation of the tax base for VAT related to previous tax periods, and there is no fact of non-reflection or incomplete reflection of information, therefore, there are no grounds for submission a revised declaration to the tax authority in the manner prescribed by Art. 81 of the Tax Code of the Russian Federation.

If the invoice is issued by the seller in one tax period, and is received by the buyer in the next tax period, then the tax deduction may be made in the tax period in which the invoice is actually received (paragraph 2, clause 1.1 of article 172 of the Tax Code of the Russian Federation, p. 2 of the Rules for maintaining a purchase book used in calculating value added tax, approved by Resolution N 1137). To do this, it is advisable to record the moment of receipt of such an invoice (register in the journal of received and issued invoices, the journal of incoming correspondence, attach an envelope and postal (courier) marks, etc.).